Bloomberg Commodity Index: Oil Ready to Pop as Coffee Perks up and Gold Takes a Breather

Ole S. Hansen, Head of Commodity, shares his insights into the current trends in commodity market

Head of Commodity,

Strategy at Saxo Bank

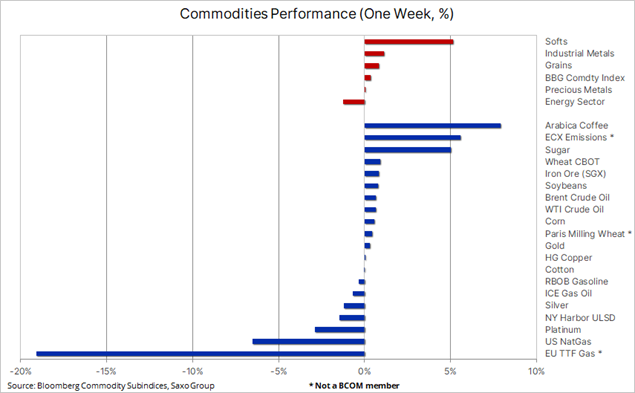

The Bloomberg Commodity Index (BCOM) traded higher for a third week as it continued to recover from an early January selloff that was driven by the IMF’s global recession warning. Gains were broad, although the energy sector was being weighed down by continued weakness in natural gas as prices slumped to their lowest since June 2021.

The themes underpinning prices remain the same, with financial markets seeing a softer dollar and lower yields in anticipation of the US Federal Reserve moving closer to pausing an aggressive rate hike cycle. Since starting last March, this has driven the US Fed Funds rate up to 4.5% with the market now pricing in less than two 25 basis point rate hikes before the pause.

The demand side, apart from the risk of a slowing global economy, is being supported by the prospect of China’s reopening – driving expectations for a pick-up in demand for commodities from the world’s biggest consumer of raw materials. However, with the prolonged shutdown of markets in China during the Lunar New Year holiday, some recent strong gainers, such as copper, iron ore and crude oil paused, thereby allowing other commodities to appear at the top of this week’s leaderboard. In the coming weeks, the risk to supplies of Russian fuel products may add an extra layer of support for gasoline and not least diesel, thereby providing enough support to keep crude oil shielded from recession-related demand fears.

The BCOM agriculture sector index was heading for its highest weekly close in nearly three months and, following a troubled start to the year, both the grains and soft sectors showed signs of bottoming out, as improved fundamentals helped reign in some elevated short positions held by hedge funds – especially in wheat and coffee.

China reopening drives biggest monthly jump in Australian stocks since 2020

Australia’s equity market – considered a dividend and commodity play as well as an investment proxy for China’s reopening given its heavy exposure to financial and materials companies – has recorded its biggest monthly gain since November 2020, up 6.5% so far this month. Mining giant BHP Group expects 17% dividend growth, with iron ore miners forecasting higher demand for high-grade iron ore from China, which supports higher earnings. Despite a lull in activity during China’s Lunar New Year holiday, iron ore, the steel making ingredient, hit a six-month high at $128 a ton on the Singapore futures exchange (SGX) this week. This was not only driven by expectations China will increase buying after the Lunar New Year holiday, but also because Australia’s largest pure play iron ore company, Fortescue, expects stronger sales in the first half of 2023.

Wheat consolidating above key support with rice at a two-year high in Asia

Chicago wheat, one of the three most shorted commodities by hedge funds together with Arabica coffee and natural gas, traded higher on short covering as crop conditions worsened in Texas, the second biggest US producing state of winter wheat. In addition, short-term weather forecasts point to frigid wintry weather across the US Midwest next week, raising the risk of winterkill in areas without protective snow cover.

Lower supply of corn and wheat from the Black Sea region this year is likely to attract increased attention in the coming months. Ukraine anticipates its 2022 corn production at 22-23 million tons, down from 41.9 million tons in 2021, while wheat production is estimated to have fallen to about 20 million tons last year. Reduced planting due to the ongoing war could see those numbers slashed further in 2023 to 18 and 16 million tons respectively.

Before these latest supportive developments, the front month wheat futures contract for March delivery had touched its lowest since September 2021, in the process attracting the biggest speculative net short since May 2019. Having once again found support in the key $7 per bushel area, wheat could see further strength and short covering on a break above $7.6 ahead of $8.

Due to disrupted wheat supplies from Ukraine and strong demand, Thai rice, a benchmark for Asia, has soared to its highest in almost two years. Rice is a staple for half the world, and while wheat soared to a record in March last year, rice was subdued for most of 2022, constraining food inflation in Asia. Meanwhile, the Rough Rice contract traded in Chicago is up 21% year-on-year and, apart from a brief covid outbreak spike in 2020, trades near a 14-year high.

Coffee strikes back at short-selling hedge funds

Arabica coffee futures in New York traded sharply higher, supported by Robusta coffee’s climb to a three-month high in London above $2,000 per tons after exchange-monitored stock levels dropped to lowest since 2016 due to robust demand. In New York, the high-quality Arabica variety traded higher for a tenth consecutive day after having slumped to $1.42 per pound, a 20-month low. Months of selling on recession fears, and exchange-monitored stocks rising from a +20 year low, helped attract speculative selling from hedge funds. This culminated in the week to January 17 when the net short jumped 34% to 40.5k contracts, the highest since November 2019 and representing a nominal value of $2.4 billion. It highlights the risk of a sudden turnaround when overextended positions suddenly meet a change in the technical and/or fundamental outlook.

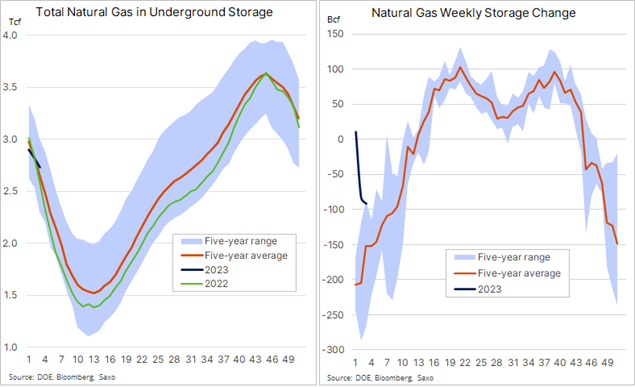

US natural gas slumps to April 2021 low on ample supply

Global natural gas prices continue to slump with heavy losses seen on the futures markets this month, as a combination of ample supply and mild winter weather reduced demand for heating. While the European TTF benchmark gas contract has lost 30% this month – and is currently trading near a 16-month low close to €50/MWh ($16/MMbtu) – US natural gas has slumped below $3/MMBtu to its lowest since April 2021, mostly on healthy supply as daily production continues to exceed 100 billion cubic feet (bcf). This has resulted in smaller than expected weekly storage reductions with the latest weekly withdrawal of 91 bcf being less than half the seasonal average of 190 bcf. In addition, Freeport LNG’s long-shut LNG export plant in Texas has started receiving small amounts of pipeline natural gas as it prepares to reopen after an explosion last June removed 20% of US export capacity.

Brent crude stumbles ahead of $90 but support remains firm

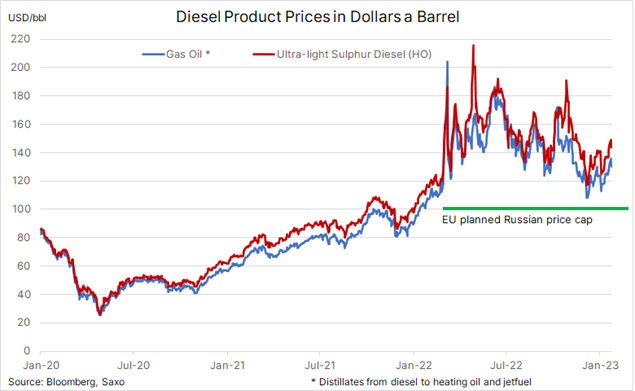

Crude oil trades near unchanged on the month and while recession risks remain and, in some places, have strengthened, the market has managed to find support from an expected increase in Chinese demand and supply concerns related to the February 5 introduction of an EU embargo on Russian seaborne sales of fuel products.

Once the EU embargo on Russian seaborne fuel exports kicks in, we are likely to see prices for gasoline and especially diesel remain supported by tightening supply – not least if the embargo is being followed up by a $100 per barrel price cap on diesel, a level that is some $30 below current market price. Russia may, however, struggle to offload its diesel to other buyers, with key customers in Asia being more interested in feeding their refineries with heavily discounted Russian crude, which can then be turned into fuel products selling at the prevailing global market price.

Supply of diesel to Europe from the US and the emerging refinery hub in the Middle East may make up some of the missing barrels from Russia, but a shortfall seems likely, not least considering the prospect for a strong recovery in China leading to lower export quotas. In addition, the recovery in jet fuel demand will pressure diesel yields, thereby creating another layer of support for distillate cracks on either side of the Atlantic.

Brent is currently trading within a $9-wide up-trending channel within a medium-term downtrend, both offering firm resistance in the $89-$90 area. A breakthrough is likely to send the market higher towards the 200-day moving average, currently at $97.50. Ahead of channel support at $80.35, some support is likely to be provided by the 21- and 50-day moving averages, currently around $83.50.

Gold pausing after hitting fresh cycle high

Gold traded close to unchanged on the week, but not before reaching a fresh cycle high at $1950, driven by demand from speculators and investors seeing an improved outlook. Last year’s headwinds are becoming tailwinds, as rate hikes eventually pause and yields and the dollar soften amid concerns about the economic outlook. This past week, traders have also moderated their estimates for how low inflation will eventually drop. This change is driven by the realization that some inflation measures are not that easy to kill, despite the inflationary dampening impact of the current rate hike cycle.

However, given gold’s steep ascent during the past two months which has seen it rally some $330 above the November low, the need for a period of consolidation is long overdue. Whether it is consolidation or correction will depend on the yellow metal’s ability to hold trendline and the 21-day moving average both currently around $1890.

Notwithstanding changes in the dollar and yields – both key directional drivers for algorithmic trading systems – we are watching ETF holdings, which reached an 11-week high following a modest increase this past week, the mentioned rise in US breakeven and inflation swap rates, and not least next week’s FOMC meeting to gauge further insights into the thinking at the world’s most important central bank.

Apart from this week’s high at $1950 and $1963, the 76.4% retracement of the 2022 correction, there is no major level of resistance before the psychologically important $2000 level, while support is well defined around $1900 where the 21-day moving average line meets the ascending trendline from the November low.